FOMC Preview: Doves to Take the Reins?

Fed Gets More Dovish In Reaction Function

During the 3 May FOMC meeting, the Fed made it clear that they were still planning on tightening the monetary policy, but not as much as previously anticipated. Chair Jerome Powell did not say that a June hike wouldn't happen and emphasized that future decisions would be based on the most recent data available and discussed at each meeting.

Afterward, the information demonstrates that there hasn't been any improvement in disinflation. Additionally, growth is still greater than expected, and the credit crisis doesn't seem to have affected growth significantly. However, Vice Chair Philip Jefferson has indicated that the Federal Reserve is planning to avoid raising interest rates during the June meeting. Jefferson made this statement during a speech he gave on May 31st.

I believe that this indicates a shift towards a more cautious approach, which shows the increasing power of those who are more hesitant within the FOMC. This is in part due to Governor Jefferson being nominated as Vice Chairman. In recent weeks, Jefferson's statements have become more hesitant than confident, even though there have been several indications of positive economic growth.

Adriana Kugler's appointment to take over Governor Jefferson's position is expected to strengthen the doves' stance within the FOMC. Professor Kugler, just like San Francisco Fed President Mary Daly, specializes in labor economics. As a result, she may prioritize employment over inflation in fulfilling the Fed's mandate.

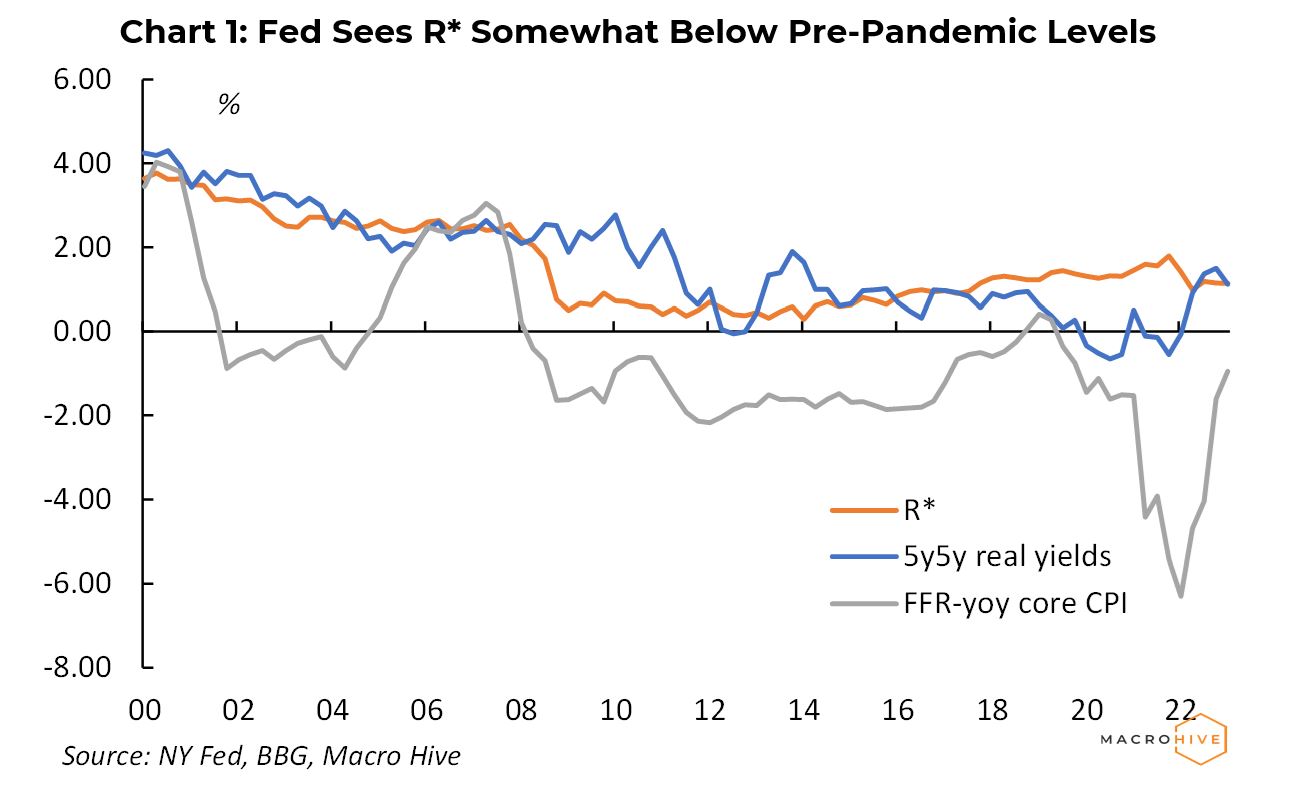

Another indication that the Federal Reserve Open Market Committee is leaning towards a more cautious approach is the statement made by New York Federal Reserve President John Williams. According to Williams, there is no proof that the time of very low natural interest rates has come to an end. His approximation of R* is at 1.1%, a decrease of around 25 basis points compared to its level in Q4 2019 (Chart 1). Additionally, Williams forecasts that R* will drop below zero by the conclusion of 2024, based on the Blue Chip predictions of inflation, GDP, and interest rates.

Williams has failed to clarify how the current status of monetary policy corresponds to his evaluations of R*. Specifically, he has not specified which gauge of inflation he favors for analyzing the actual interest rate. Currently, the 5y5y TIPS yield is at 1.4%, while the simpler Federal Funds Rate minus the headline CPI stands at only 0.2%.

However, his perspective that the age of low R* hasn't concluded gives some shelter for the Federal Reserve's cautiousness. Moreover, his prediction that R* will decrease approximately 125 basis points by the conclusion of 2024 possibly implies more interest rate reductions in 2024 than the 75 basis points presented in the March SEP. Coincidentally, I have the same doubts as the Bank for International Settlements about the factual and rational basis of R*.

I am not anticipating any significant alterations to the statement or the median dots. I foresee minor modifications to the first section on the economic evaluation, and the paragraphs discussing the risks of a credit crunch and policy position remain unchanged.

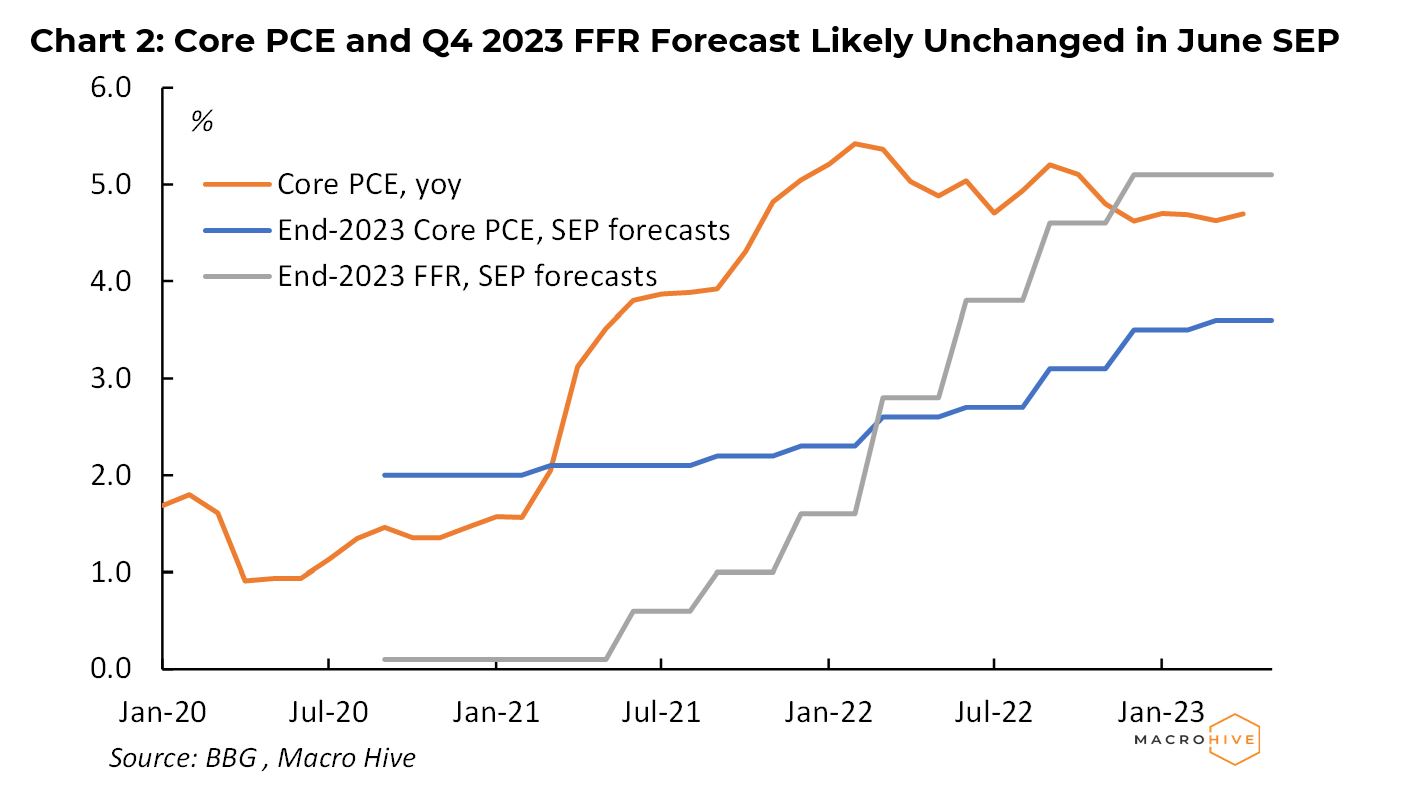

Overall, I don't think the median dot will go up. This is because it would have to be based on the FOMC's prediction of Q4 2023 core PCE, which is currently at 3.6% (according to Chart 2). Honestly, I think there's less than a 10% chance that core PCE will actually get to that level, especially since it's currently at 4.7%. But I don't think the FOMC will give up and say they were wrong just yet. I think it's more likely that they'll adjust their forecast and predict that the core PCE will actually increase, along with the 2023 FFR, in the September SEP.

The members of FOMC have frequently emphasized that reducing interest rates this year goes against the gradual decrease of inflation that FOMC has envisioned. I share the same opinion.

Currently, the market estimates that there is an 80% likelihood that a complete hike will take place between the meetings in June and July. However, taking into account the Fed's more cautious approach, I think the chances are around 55%.

As I don't anticipate a notable decrease in inflation for the rest of the year, my prediction remains that the Federal Reserve will increase interest rates twice more before December ends.