Huadi International Group (NASDAQ:HUDI) Will Be Hoping To Turn Its Returns On Capital Around

If we are searching for a stock that has the potential to greatly increase in value over a long period of time, what indicators should we consider? Among other factors, we should look for two main things: firstly, a rising return on capital employed (ROCE), and secondly, an increase in the company's total capital employed. If we observe these trends, it usually suggests that the company has a strong business model and numerous opportunities for profitable reinvestment. However, upon examining Huadi International Group (NASDAQ:HUDI), we do not believe that its current trends align with those of a stock that has the potential for significant future growth.

Decoding ROCE: Unveiling Capital Efficiency

To provide further clarification in case of any uncertainty, the ROCE serves as a measurement to assess the percentage of pre-tax income that a company generates from its invested capital. Analysts utilize this equation to compute the ROCE for Huadi International Group.

Return on Capital Employed can be calculated by dividing the earnings before interest and tax (EBIT) by the total assets minus the current liabilities.

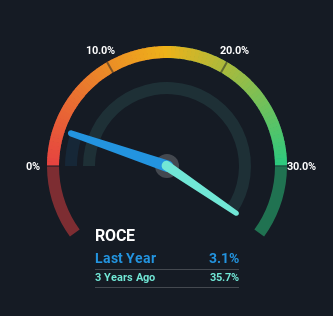

0.031 equals 2.5 million US dollars divided by the difference between 98 million US dollars and 17 million US dollars, based on the twelve months leading up to March 2023.

Consequently, Huadi International Group is achieving a return on capital employed (ROCE) of 3.1%. Ultimately, this figure represents a subpar performance compared to the average ROCE of 10% within the Metals and Mining industry.

Take a look at our most recent examination of Huadi International Group

Although the future may not mirror the past, it can be beneficial to have knowledge of a company's previous performance. That's why we have provided the chart above. If you want to delve into Huadi International Group's historical performance, feel free to explore this complimentary visual representation of their past earnings, revenue, and cash flow.

The ROCE Trend's Insight

At first glance, the ROCE trend at Huadi International Group does not give a strong impression. In the past five years, the returns on capital have significantly dropped from 46% to 3.1%. However, it seems that Huadi International Group is focusing on long-term growth by investing more capital, even though their sales have remained relatively stagnant in the past year. It may take a while before the company begins to witness any significant financial benefits from these investments.

In addition, Huadi International Group has managed to lower its present debts to comprise only 18% of its overall assets. This marks a substantial decline from the previous ratio of 82%, and is likely the reason behind the decrease in Return on Capital Employed (ROCE). Furthermore, this reduction in liabilities can potentially mitigate certain risks faced by the company, as it relies less on suppliers and short-term creditors to fund its operations. However, others might argue that this change hampers the company's efficiency in generating ROCE, as it now relies more on its own funds to support its operations.

Combining everything, although we find it promising that Huadi International Group is putting money back into its own company, we acknowledge that profits are dwindling. Additionally, with the stock declining by 78% in the past year, it seems like investors are anticipating negative outcomes. In any event, this stock doesn't possess the characteristics of a highly lucrative investment that were mentioned earlier. Therefore, if you're seeking such an opportunity, we believe you'd have better chances elsewhere.

Additionally, it is worth noting that we have noticed three indicators that raise concerns about Huadi International Group. At least one of these indicators has made us feel slightly uneasy. It would be beneficial to comprehend these warning signs.

Although Huadi International Group may not be generating the highest profits, take a look at this complimentary compilation of companies that are achieving commendable returns on equity, supported by sturdy financial standing.

Do you have any thoughts about this article? Are you worried about the information in it? Contact us directly if you do. Alternatively, you can send an email to the editorial team at editorial-team (at) simplywallst.com.

This blog post from Simply Wall St is written in a broad and universal manner. We offer our perspectives using objective methods by relying solely on past information and expert predictions. Our posts should not be considered as financial guidance and do not suggest either buying or selling any specific stocks. They do not consider your specific goals or financial circumstances. Our objective is to provide in-depth analysis that focuses on the long-term outcomes based on fundamental data. It is important to note that our analysis may not account for the most recent company announcements or subjective material. Simply Wall St holds no investment positions in any stocks mentioned.